Data Modernization in Financial Services:

Where Most Projects Go Wrong

Financial services firms invest heavily in data modernization, yet consistently underestimate the difficulty of execution. Our perspective examines the most common failure patterns across banking,

insurance, and wealth management, and provides a diagnostic checklist for CIOs and CTOs to avoid them.

Financial institutions understand the imperative. The evidence is in the budget lines, the board presentations, and the technology roadmaps. Banks, insurers, and asset managers have been approving data modernization programs for the better part of a decade, and the pace of investment has accelerated sharply as AI ambitions have raised the stakes on having a data infrastructure that can support more than batch reporting.

Yet the outcomes tell a different story. According to Deloitte’s State of Generative AI in the Enterprise survey, only one quarter of banking respondents said their data management platforms are highly or very highly prepared to adopt generative AI tools and applications. For organizations that have been modernizing for years, that figure is striking. It suggests that investment volume is not the variable that determines whether a data modernization program produces a fit-for-purpose platform. Something else is failing.

Nearly six out of ten banking leaders surveyed in a Forbes Insights report identified legacy infrastructure as the top challenge impeding their organization’s business growth. That figure has not meaningfully changed in several years. The recognition of the problem is near-universal. The execution remains consistently short of what programs are designed to deliver.

This article examines the structural reasons across banking, insurance, and wealth management, and provides a checklist for CIOs and CTOs to diagnose and address failure patterns before they become program postmortems.

The Financial Services Context Is Unlike Any Other Industry

Before addressing the failure patterns, it is worth being precise about why data modernization in financial services is structurally harder than in other industries. It is not merely that financial institutions have older systems. It is those systems that are embedded in regulatory, operational, and risk frameworks that make changing them consequential in ways that do not apply in most other sectors.

A bank’s core banking system does not just process transactions. It is the authoritative source for regulatory capital calculations, AML reporting, customer identity verification, and interest accrual logic, validated over years of regulatory examination. A change to that system is not a technology project in isolation. It is a risk event that compliance, audit, legal, and the regulators themselves are interested in.

In fiscal year 2024, US financial regulators issued significantly more enforcement actions for Bank Secrecy Act and AML violations than in the previous year, and banks submitted a record 2.6 million suspicious activity reports, an average of 7,100 per day. The regulatory environment is not softening. It is intensifying. And the data infrastructure that supports compliance reporting is, in many institutions, the same infrastructure that is being asked to support real-time analytics, fraud detection, and AI model serving simultaneously. Those are fundamentally incompatible demands on a legacy architecture. The system cannot serve all of them reliably, and in most institutions, the consequence is a modernization program that gets deferred, descoped, or stretched well beyond its original timeline.

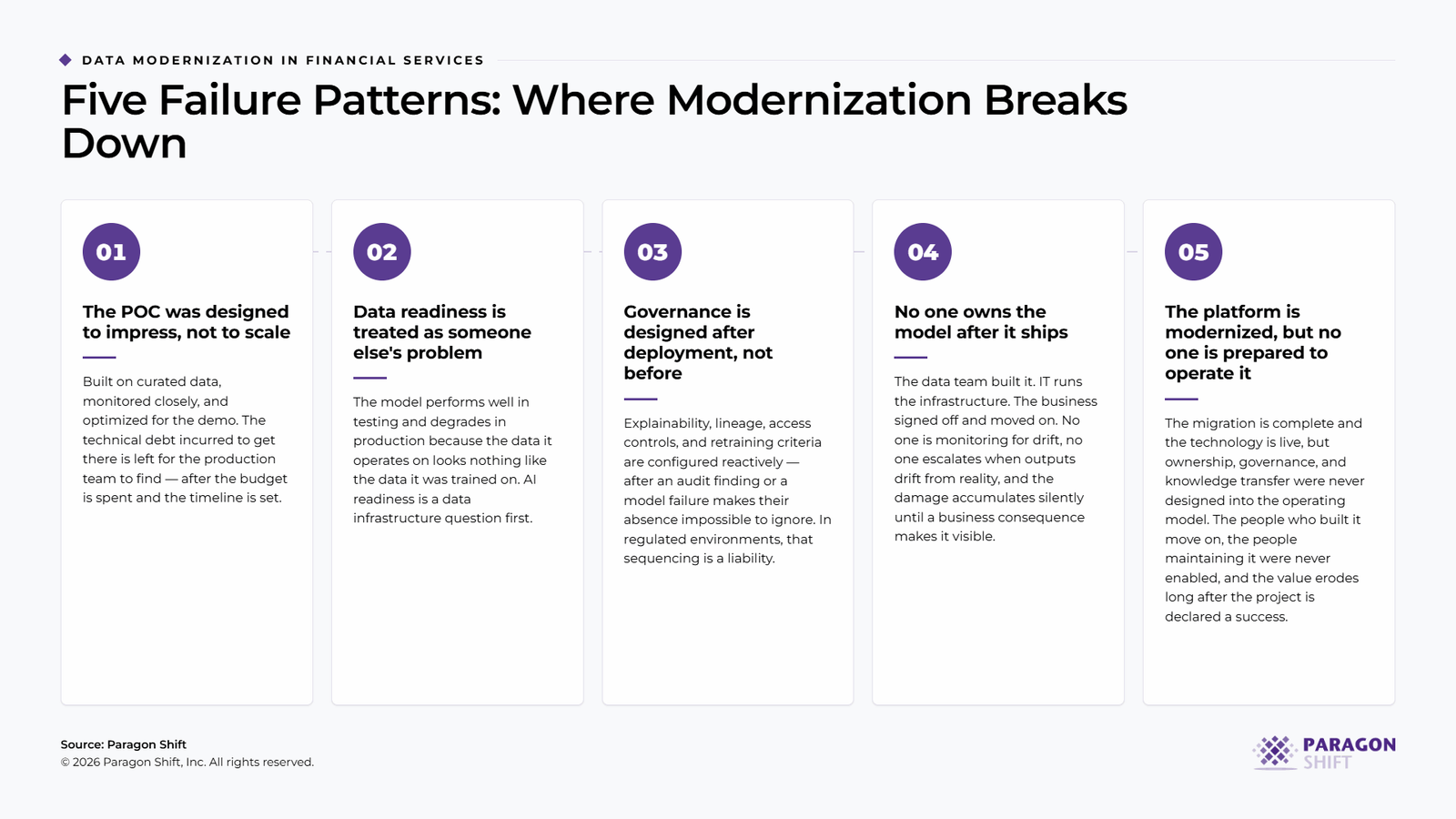

Failure Pattern 1: Treating Modernization as a Technology Project Rather Than a Business Program

The most common failure pattern in financial services data modernization is also the most foundational. The program is owned by IT. The business units are consulted during requirements gathering. The success criteria are defined in technical terms. And 18 months into an 18-month program, the business units are not using what was built because the output does not answer the questions they need answered.

This is considered a governance failure. The program was designed to modernize the data platform, not to improve the specific analytical and operational capabilities the business relies on. Those are related but not identical objectives, and conflating them produces technically successful migrations that generate no measurable business value.

Gartner predicts that 80 percent of data and analytics governance initiatives will fail by 2027 due to the absence of a genuine or manufactured crisis that forces organizational alignment. The implication for CIOs is that governance cannot be designed as a technical framework and handed to the organization as a policy. It has to be anchored to a business outcome that the relevant stakeholders have a stake in protecting.

In banking, the failure pattern is visible in mortgage origination environments where the loan operations team continues to pull data from the core banking system directly rather than from the new data platform, because the new platform does not reflect the business rules they trust. In insurance, it shows up in claims departments that maintain their own data extracts because the enterprise data warehouse refreshes overnight, and their work requires intraday accuracy. In wealth management, it appears when portfolio management teams build parallel reporting in spreadsheets because the enterprise BI environment does not support the investment attribution methodology their clients expect.

In each case, the data platform was built. The business did not adopt it. The reason is the same: the platform was designed around the technology problem rather than the operational one that the business needed it to solve.

The fix requires starting every data modernization program with a clearly defined set of business outcomes, including specific decisions that will be made differently, specific processes that will operate faster or with fewer errors, and tracing every architecture decision back to whether it advances or impedes those outcomes.

Failure Pattern 2: Underestimating the True Cost and Scope of Legacy Debt

Financial services organizations consistently underestimate the complexity embedded in their legacy systems, and that underestimation drives the most expensive form of project failure: the program that discovers its actual scope 18 months into a 12-month plan.

The hidden complexity is typically not in the data itself. It is in the business logic embedded in the systems that produce the data. Core banking platforms, policy administration systems in insurance, and portfolio management systems in wealth management accumulate decades of business rules encoded in stored procedures, transformation logic, and application code. Some of that logic has no documentation. Some of it is understood only by people who are no longer in the organization. All of it needs to be understood, extracted, and re-implemented correctly before the modernization can be considered complete.

Deloitte’s analysis of banking legacy modernization identifies the capture of institutional knowledge locked in legacy systems as one of the most critical and consistently underestimated phases of any modernization program. Business rules that exist only in the system or in the institutional memory of long-tenured employees represent intellectual property that cannot be reconstructed after the fact if it were lost during migration.

For insurance companies, the challenge is compounded by product complexity. A personal lines insurer running products that have been in force for twenty years may have rating algorithms, coverage modification rules, and claims handling logic embedded in policy administration systems that predate current regulatory requirements. Migrating that logic to a modern platform is not a data migration. It is a business rules extraction and re-implementation program, which requires the involvement of actuaries, compliance officers, and product managers in addition to data engineers.

The practical implication for CIOs is that discovery, the structured audit of what business logic exists, where it lives, and how it connects to downstream processes, is the most important phase of any financial services data modernization program. Organizations that compress discovery to accelerate the build consistently discover in production what they should have found in assessment.

Failure Pattern 3: Sequencing Governance After Migration Rather Than Before

Data governance in financial services carries regulatory weight that does not exist in most other industries. A bank that migrates its customer data to a cloud data platform without a fully designed access control model, lineage documentation, and data residency framework not only faces an operational risk, but also a compliance exposure that regulators can and do act on.

Gartner’s 2024 research on data governance found that organizations treating governance as a tactical, data-only exercise rather than as a business-centric model that addresses decisions, processes, and outcomes are far more likely to fail to achieve their governance objectives. In practice, this manifests as programs that build a data catalog after the platform is live, configure row-level security after the first audit finding, and document data lineage only when a regulatory inquiry makes the absence of that documentation a legal issue.

The sequencing failure is understandable. Governance work is slower and less visible than engineering work. It does not produce a demo or a dashboard. It does not satisfy the executive stakeholder who wants to see progress at the quarterly review. And in organizations where the data modernization program is being driven by a platform migration deadline rather than a business capability objective, governance is the first workstream to be deprioritized.

The cost of that deprioritization is substantial. Research on banking technology transformation found that organizations with legacy infrastructure typically spend 4.7 times more on compliance for those systems versus modern alternatives, and that the compliance cost differential widens each year modernization is delayed. When governance is not designed correctly in the target state, the new platform inherits the compliance burden of the legacy environment rather than reducing it.

For asset managers operating under SEC data management requirements, for banks subject to BCBS 239 principles for risk data aggregation, and for insurers navigating state-level data privacy regulations, the governance framework is not an optional enhancement to the data platform. It is a precondition for the platform being legally permissible to operate.

At Paragon Shift, the data modernization engagements we conduct in financial services always establish the governance framework, including access controls, lineage requirements, sensitivity classification, and data residency decisions before architecture design begins. The governance requirements determine the target architecture, not the other way around. Organizations that reverse this sequence consistently find themselves redesigning the architecture after it is built to accommodate governance requirements that were not factored in at the design stage.

Failure Pattern 4: Migrating the Problem Rather Than Solving It

Migration programs have a natural bias toward fidelity. The objective is to migrate data from the legacy environment to the modern platform accurately and completely. That objective, pursued without a critical evaluation of what is being migrated, creates modern platforms that replicate the structural problems of the legacy environment in new infrastructure.

The most common version of this failure in banking is migrating a data warehouse that was built for a batch reporting cycle to a cloud environment and running the same batch pipelines on cloud infrastructure. The organization has modernized the platform but not the architecture. The reports are still stale by the time leadership sees them. The close cycle is still long. The business rules are still embedded in stored procedures rather than in a governed semantic layer. The only thing that changed is the vendor invoice.

Deloitte’s 2025 banking outlook specifically flags this pattern: deploying AI or modern data platforms more widely and successfully will not happen unless leaders address how, and to what extent, their banks continue to rely on disjointed and antiquated legacy technology infrastructure contributing to technical debt. Simply moving that infrastructure to a cloud environment does not resolve the underlying architectural debt.

In the insurance industry, a parallel pattern appears in claims data migration programs. An insurer that migrates its claims database to a modern cloud warehouse without redesigning the data model ends up with a modern platform that cannot support the real-time claims triage and fraud detection the business was hoping to enable, because the data model was designed for batch reporting rather than event-driven processing. The business case promised near-real-time fraud detection. The architecture delivered a faster version of the same batch process.

The migration program should be the trigger for the architecture redesign, not a prerequisite. Deciding which elements of the legacy architecture to carry forward and which to redesign is one of the most consequential judgment calls in a financial services data modernization program. It requires both technical depth and business context, an understanding of which legacy patterns encode genuine business requirements and which are artifacts of the constraints of thirty-year-old technology.

Failure Pattern 5: Insufficient Talent and Operating Model for Post-Migration Sustainability

The final failure pattern is the one that most program retrospectives do not surface until well after the fact. The organization successfully modernizes its data platform. The migration is complete. The new environment is live. And then, six months later, the platform is not being maintained to the standard the program intended, because the people who built it have moved on, and the people operating it were not designed into the operating model from the beginning.

In regional and mid-market financial institutions, this talent constraint is structural. The institution lacks the engineering depth to maintain a modern data platform at the standard of a tier-one bank. The program was designed by consultants who are no longer available. The documentation is incomplete. The data quality monitoring that was designed at the architectural stage was never fully implemented because the program ran out of time in the final sprint.

The Bank Director 2025 Technology Survey found that one-third of bank leaders cited ineffective use of data as a major obstacle to success, even among organizations that had completed significant technology modernization programs. Modernization without a sustainable operating model produces a capable platform that the organization cannot fully exploit, which generates exactly the kind of executive frustration that makes the next modernization program harder to fund.

The operating model question around who owns the data platform post-migration, how quality is monitored, how the governance framework is maintained as data volumes and sources grow, and how the platform evolves to support new business requirements needs to be answered before the program is designed, not after it is delivered.

At Paragon Shift, our Data Modernization practice in financial services addresses this through a structured knowledge transfer and operating model design phase that runs in parallel with the technical build, not as an afterthought at program close. The organizations that sustain the value of their modernization investments are the ones that plan for operations from day one of the program design.

A Diagnostic Checklist for CIOs and CTOs

Before approving or continuing a financial services data modernization program, the following questions should have documented answers. The absence of a clear answer to any one of them is a program risk.

- Is the program owned by a business leader with accountability for the operational outcomes it is meant to produce, or does IT own it with business stakeholders in a consulting role?

- Has a structured discovery of legacy business logic been completed, with an explicit accounting of what rules exist, where they live, and what the migration strategy for each is?

- Has the governance framework, including access controls, lineage documentation, data residency, and sensitivity classification, been designed and approved before the architecture design is finalized?

- Is the architecture being redesigned for the requirements of the target state, or is it replicating the structure of the legacy environment in modern infrastructure?

- Is there a post-migration operating model with defined ownership, quality monitoring standards, and a talent plan that does not depend on the program team remaining in place?

These are not complex questions. They are the questions that programs with the best outcomes in financial services can answer clearly at the start of the engagement. The programs that cannot are the ones generating the statistics cited at the beginning of this article.

Key Takeaways

1. Data modernization failure in financial services is predominantly structural and organizational, not technical. The platform capabilities are available. The sequencing, governance, and ownership decisions that determine whether those capabilities are realized are where most programs fall short.

2. Discovery, the structured audit of legacy business logic and embedded rules, is the most consistently underestimated phase of any financial services data modernization program. Compressing it to accelerate the build is the single most reliable predictor of scope overrun.

3. Governance must be designed before architecture in regulated financial services environments. Access controls, lineage, and data residency requirements determine what the target architecture is permitted to look like. Programs that reverse this sequence redesign their architecture twice.

4. Migration is not modernization. Moving legacy data and processes to cloud infrastructure without redesigning the architecture replicates the structural problems of the legacy environment at a lower hardware cost.

5. Sustainable value from data modernization requires a post-migration operating model with defined ownership, quality standards, and a talent plan. Programs that treat operating model design as a post-delivery activity consistently underperform against their original business case.

Conclusion

The data modernization imperative in financial services is not going to diminish. Regulatory expectations for data quality and auditability are rising. Competitive pressure from institutions that have successfully modernized their data infrastructure is visible in product velocity and customer experience. And the AI capabilities that boards and executive teams are expecting to deploy depend entirely on the quality of the data foundation beneath them.

The organizations that will close the gap between modernization investment and outcome are not the ones that approve larger budgets or adopt newer platforms. They are the ones who diagnose the structural failure patterns before they become program problems and design the governance, sequencing, and operating model that those patterns demand.

If your organization is preparing for or is currently navigating a data modernization program in financial services, Paragon Shift’s Data Modernization practice brings direct experience in financial services environments across banking, insurance, and wealth management.